This Season is one of reflection and re-dedication for me, with the two-month transition from Emancipation Day on 1 August to Independence on the 31 August, then onto Republic Day on 24 September. I always spend this spell in some sober reflection, in between the life. It seems to me that the very sequence of events and the consequent holidays in the season imbue it with an inner meaning in terms of a national transition to some kind of depth and purpose. Emancipation to Independence to Republican status…this is my Season of Reflection, maybe that is just sentimental of me, but let us see.

This summarises the reply of Ministry of Finance PS Dhanpaul on 14th June 2018, to my original request of 24th April 2018. Dhanpaul wrote that the Ministry –

had no details of legal fees as the lawyers were not retained by them;

had no CLF audited accounts from 2008 to date, but management accounts for 2015, 2016 and 2017 were sent;

denied my request for the presentation made to Independent Senators in September 2011 on the grounds that since we had agreed to omit that item from the Consent Order my request was ‘an abuse of the process of the court‘. In any case the file could not be located.;

Legal and other advice was being obtained on the outstanding items;

Further letters were to be sent via hard-copy, other formats would be ignored.

Email

From – Afra Raymond

To – Vishnu Dhanpaul

Date – Fri, Jun 22, 2018 at 7:42 PM

Hello PS Dhanpaul,

I have carefully considered your reply of 14th June 2018, the overall tone and content of which is perturbing, given the background in this matter.

My reply is itemised here for ease of reference –

The group accounts for CL Financial – Thank you for providing the management accounts of CL Financial Limited as at December 31st 2015, December 31st 2016 and April 30th 2017. Of course the 2015 accounts show balances for 2014, so what is the document from which those 2014 numbers were derived? My original request was for ‘…audited accounts of CL Financial Limited…to include interim, preliminary, draft, unaudited or management accounts…‘. Those broad request terms were submitted precisely to allow for the related matters of opening balances and source documents to be accommodated. In light of that, please provide the set of accounts from which the 2014 balances were taken, whatever the permutations in which those might appear. Also, please provide the available accounts for the outstanding years – 2008 to 2014 – whether those be interim, preliminary, draft, unaudited or management accounts;

Legal Fees – Please reply to indicate which Ministry or State Agency had responsibility for retaining and paying the attorneys who represented the Ministry of Finance in these two court case – I find your answer to be verging on the obtuse;

Presentation to Independent Senators made in September 2011 – The consent order of 24th January 2018 in no way affects that this document is disclosable – indeed, the Ministry’s 22nd January 2018 Supplemental Submission set out a clear position, which accepted that there are no applicable exemptions in the FoIA to prevent publication of the presentation made to Independent Senators in September 2011. Its twelfth paragraph states – “…As to the Order in relation to Request No. 2 the Appellant’s position is that it accepts that there is no exemption on which the Appellant can rely…” For your information, a copy of that document is hyperlinked above for ease of reference. In the circumstances, the Ministry’s position is risible in that even if one accepts its position, which I do not, any other applicant would be entitled to obtain the document without that defence being available. In any case, a presentation of that importance would have been the subject of considerable email traffic, which means that there would have been drafts and attachments exchanged between the Ministry and its advisers – those email records need to be examined for those documents. Your suggestions as to an abuse of process are quite misplaced and somewhat ironic, given my next point;

The outstanding items – The issue of the details of the costs of the CL Financial bailout was litigated since March 2013, with the Ministry having lost at the High Court in July 2015 and conceded defeat at the Appeal Court in January 2018. What could possibly be your rationale for seeking further legal and other advice on these requests? This series of requests for information is being made to the same Public Authority in respect of the same bailout process, the only material difference being that the information being requested now was not previously requested. This series of requests is being made, in the public interest, to obtain the outstanding details of exactly how this bailout was funded. By way of illustration and for the benefit of other readers, take the case of a request for information under the FoIA which sought certain details of applicants for certain state training with names from A-F. In that example if the application was refused, then became the subject of judicial review, then the High Court ruled in favour of the publication and the State conceded its case at Appeal Court level, how then could the State refuse a subsequent application for the same details of applicants for the same training program with names G-Z? It is my considered view that for a Public Authority to be seeking further legal and other advice in such a situation would be tantamount to an abuse of process. I am stating that for the benefit of any other readers who might be unclear as to the important principle at stake in this matter. I have no doubt that you fully understand the issues as stated. Quite apart from the commitment of scarce public resources to obtain further advice on this matter, please note that the Ministry is now beyond the 30-day deadline specified at S.15 of the Act to indicate whether it is refusing or approving my requests;

Communication – I reject your proposals as to our future communications. At this time, the vast majority of my communications are via email, possibly 95% – I have little doubt that the ratio is any different at the PS level of our public service. In these circumstances, what could possibly be your rationale for proposing the hard-copy mode for our further communication? In any case, all the Ministry’s letters in this current exchange are being delivered to my office, notwithstanding the typed address being my home.

I await your early reply so that this long-outstanding matter can be properly concluded, in the public interest and without any further delay. For the avoidance of doubt, please do not take this correspondence as in any way representing my acceptance of your delay, now well outside the time-limit stipulated in the Freedom of Information Act. All my rights are hereby reserved.

This article provides more details of the games being played in this Information War. It seems that the concealment of the details of the CL Financial bailout is of high importance.

First item is this acknowledgment from the PS in the Ministry of Finance which would be funny, if this entire matter were not so very serious –

This article sets out my ongoing search for all the details of all the payments made under the CL Financial bailout. That includes my recently-concluded litigation and my new requests for information under the Freedom of Information Act.

Any unaudited financial statements of CL Financial Limited for the years 2008-2011 in the possession of the Ministry of Finance which were relied upon to prepare the affidavits of Minister Winston Dookeran filed on 3 April, 2012 in High Court proceedings CV 2011-01234, Percy Farrell and Others v Clico and others.

Any list of the creditors of CL Financial existing at the date of the request in the possession of the Ministry of Finance, the names of the EFPA holders of Clico, the dates of the repayment of EFPA holders of Clico and the identities of those whose investments have been repaid.

The Ministry’s attorneys have now stated that they are unable to locate the specified financial statements and the list of CLF creditors has not been provided. My team will be responding to press for those details, in the public interest and in accordance with the Appeal Court’s Consent Order. Continue reading “CL Financial bailout – filling the gaps”→

The National Investment Holding Fund Co Ltd (NIF) was announced (p.18) on 25th June 2018 by the Minister of Finance, Colm Imbert, as an important part of the endgame of the CL Financial bailout. That announcement, which had been prefaced in earlier statements by Minister Imbert, was stated to be part of the process to recover the public money which had been spent on the CLF bailout.

The NIF is a new State-owned and controlled enterprise into which will be transferred just under $8.0 Billion in shares. About $6.0 Billion of those shares are CLF-owned – Republic Finance; WITCO; One Caribbean Media and Angostura – with a further $2.025 Billion of the State’s shares in Trinidad Generation Unlimited making up the balance. Continue reading “CL Financial bailout – the NIF matter”→

The previous article delved into the published information on the three existing State-owned hotels and juxtaposed that with the proposals for a Tobago Sandals. Apart from the unsatisfactory position with the State’s existing hotel investments and the reluctance to give details, I also updated readers on the missing MoU for the Tobago Sandals project.

My dismal readings were based on the very limited publicly-available information, nothing else. I did not refer to any rumours or ‘inside information‘, my work is all based on the published record. The PM and his colleagues surely have ready access to a better quality and quantity of information than the public. That being the case, it begs the question as to what is really happening here.

If indeed, the Sandals project has significant upsides and benefits, those ought to have been estimated and shared by now. If the existing State-owned hotels are doing well, why aren’t the management agreements or accounts published? If those hotels are doing poorly, why are we persisting with that same model? Continue reading “Property Matters – Sandals MoU? Part three”→

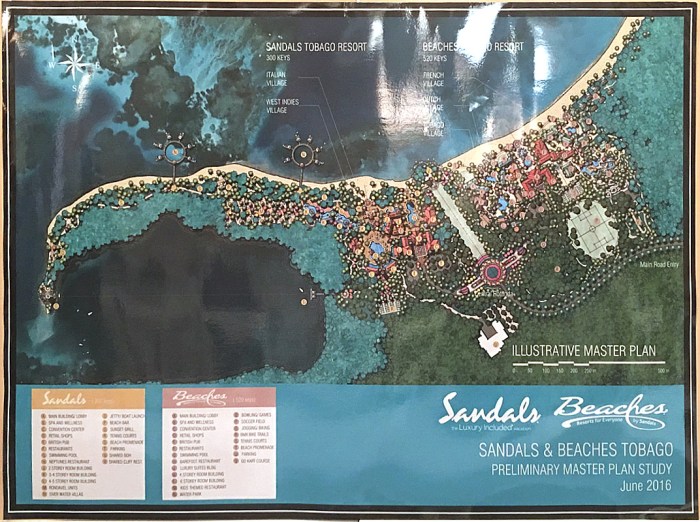

The previous article updated readers on my attempts to obtain the Sandals Memorandum of Understanding for the proposed high-end, large-scale resort development in Tobago. That proposed development is said to be a significant part of our country’s diversification efforts so it requires our sober attention if we are to understand what is at stake.

The model for this project is one in which the State either pays for or guarantees the financing of the new resort. The State would pay for the cost of design, financing, construction, fitting and furnishing of the new resort, all to the standards set by Sandals. The completed resort will then be operated by Sandals under a management agreement. T&T is unique in the Caribbean in that our largest hotels were funded by Public Money with the operators working via Management Agreements.

That is the model which has been used thus far in our State-owned hotels. That fact has been cited several times by the PM, quite likely to offer a degree of comfort to those who are unsure about this project. After all, we have done this model before, so what could be the harm if we go along the same road once more?

That approach to a major investment of this type does not offer me any comfort at all. Since September 2016 I have been pursuing a detailed research program into the State-owned hotels, with my colleagues from Disclosure Today and we have been solidly resisted. In my view, we do not have enough information about the existing State-owned hotels – Trinidad Hilton (1962); Magdalena Grand (originally Tobago Hilton, opened in 2000) and Hyatt Regency (2008) – to be confident about this approach. Continue reading “Property Matters – Sandals MoU? Part two”→

Josanne Leonard interviewed Afra Raymond on Monday 12th June 2017 on how the three parts of the state work against the backdrop of constitutional issues such as the separation of powers, the quality of representation and the size, origin and role of the Cabinet. Video courtesy Office of the Parliament

Programme Date: 22 May 2018 Programme Length: 00:21:37

My 27 February 2018 request for that MoU under the Freedom of Information Act (embedded below) was therefore made against that background of both parties’ declaration that there was no secret. The Office of the Prime Minister responded on 22 March 2018 to refuse my request, citing that the MoU contained a confidentiality clause which prevented its disclosure at this time. I have since written to the OPM to request a reply in conformity with the provisions of the Freedom of Information Act – I am still awaiting a reply to that letter.

I have now written to Mr Adam Stewart of Sandals Resorts International to request from him a copy of the MoU. (See below)

This is a proposal of high public importance as it is being advanced as an important part of our country’s diversification strategy, so the correspondence is set out in this article.

From: Afra Raymond

Date: Fri, Jun 15, 2018 at 3:41 PM

Subject: Request for Memorandum of Understanding with Sandals Resorts

To: Adam Stewart

Dear Mr Stewart,

I am writing to request a copy of the signed Memorandum of Understanding between Sandals Resorts International and the Government of the Republic of Trinidad & Tobago – it was recently reported that this MoU was signed on 10th October 2017.

There is no doubt that the proposed 750-room Sandals/Beaches Resort for Tobago will be a large-scale, high-impact development, so there an understandable public interest in those proposals. I was therefore greatly encouraged by your emphatic statements that there is no secrecy in relation to the business arrangement or the MoU and that you refuted any secret deals – as reported in the Trinidad & Tobago press on 27th February 2018.

I was therefore astonished that the Office of the Prime Minister replied on 22nd March 2018 to my request for that MoU by citing a confidentiality clause to refuse its disclosure at this time. I wrote to the OPM on 11th April 2018 requesting a clarification and their reply is still awaited. In the interim, I am requesting from you a copy of the MoU in the public interest of transparency in this large-scale development proposal.

For your information, my earlier article on the Sandals MoU was published in the Express Business on 8th March 2018 and can be accessed here. The related correspondence is attached for ease of reference.

This is the full CTV interview with Dionne Baptiste on the national housing policy and programme on 1st May 2018. Video courtesy CTV

This is the full CTV interview with Dionne Baptiste on the national housing policy and programme on 1st May 2018. Video courtesy CTV