On 17th June 2026, the Housing Development Corporation (HDC) reportedly issued its formal Notice to halt the intended award of 11 contracts totalling $3.4 Billion to build 3,700 new homes for sale, on public interest grounds.

That announcement has triggered official statements on the HDC’s intention to get the process right and to deliver these badly needed new homes for sale. All sides are going to great lengths to satisfy the Office of Procurement Regulation’s (OPR’s) requirements, so that aspect certainly represents real progress. But those statements can only offer comfort if one ignores the reality of the HDC’s extensive waiting-list, in which over 90% of the applicants can only afford to rent.

“…Whereas the People of Trinidad and Tobago—…(b) respect the principles of social justice and therefore believe that the operation of the economic system should result in the material resources of the community being so distributed as to subserve the common good…”

From the preamble of our Republic’s current Constitution (1976)

The simple truth is that the overwhelming majority of HDC’s applicants can only afford to rent, but nothing is being built for rent. That is the challenge we face in terms of realising the objectives of our Housing Policy.

I thought this would be a two-part analysis, but the final conclusions required a fuller treatment, hence this closing article to place those issues in a public policy context. My analysis led me to the conclusion that the HDC’s projects could not in any way have satisfied a proper needs assessment, as required by the Public Procurement and Disposal of Public Property Act (PPDPPA). As such, this is a call for the OPR to engage these public policy issues with the required seriousness.

The current state of play in this arena of Housing Policy and its originating Statute, operating within the PPDPPA, is plainly one in which the precept of ‘Value for Money’ is being routinely violated. HDC is a Statutory Agency, yet its vast capital spending is done in contradiction to its statutory obligations, which is the basis for my challenge as to its ability to support any value for money claims. Notwithstanding the claims of this economy or that new approach, if the HDC’s projects do not satisfy the required needs assessment, that serious failure must be the only reasonable conclusion.

These policies, laws and public agencies were intended to provide decent, affordable homes to the poor citizens in our country, in recognition of the ideal that social justice was an essential ingredient of a modern, progressive society. The historical context must first be established to understand what is at stake here.

The Housing Act, which was Act 3 of 1962, passed on August 3,1962, even before our formal Independence, which shows the importance placed on affordable housing, even in the ‘bad old days’. That Act established the National Housing Authority, which absorbed all the previous public housing agencies. Our legislators, in preparing that Act, took the care, in Section 2, to include proper definitions for –

“family of low income” means a family that receives a total family income that, in the opinion of the Authority, is insufficient to permit it to rent housing accommodation adequate for its needs at the current rental market in the area in which the family lives;

“low-rental housing project” means a housing project undertaken to provide decent, safe and sanitary housing accommodation complying with standards approved by the Authority, to be leased to families of low income or to such other persons as the Authority, under agreement with the owner designates, having regard to the existence of a condition of shortage, overcrowding or congestion of housing;

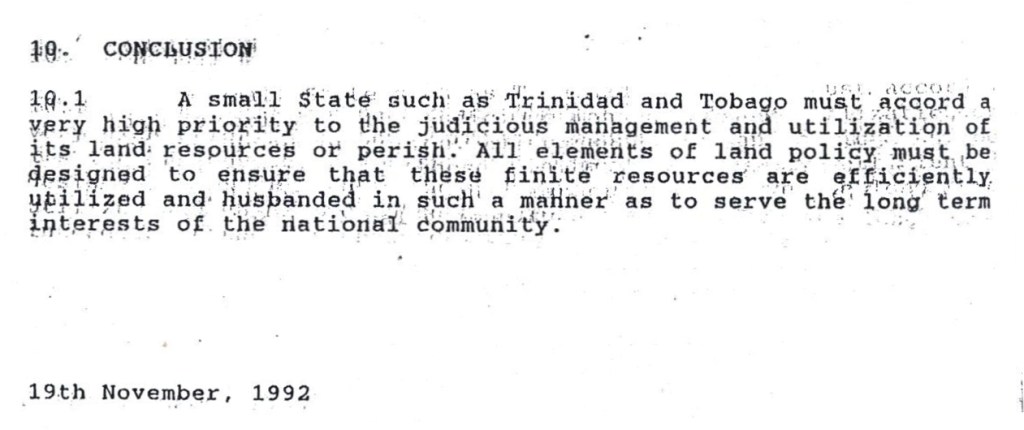

The 1992 Land Policy established strong guidelines on how our limited supply of land should be developed –

10.1 A small State such as Trinidad & Tobago must accord a very high priority to the judicious management and utilization of its land resources or perish. All elements of land policy must be designed to ensure that these finite resources are efficiently utilized and husbanded in such a manner as to serve the long term interests of the national community…

That chimes readily with the precepts of our Constitution, yet here we are, with sites being located and approved for large-scale development of new homes, all to be sold. One can scarcely recall any such official statement about sites for new homes for rent.

The 2002 Housing Policy set out the challenge of properly housing citizens who cannot afford to buy a home, and that Policy led directly to the HDC Act.

The HDC Act of 2005 – This Act established the Housing Development Corporation, which is mandated by Section 13 to create affordable homes for low and middle income applicants. The sequence intentionally sets a priority for low-income applicants, but here we are.

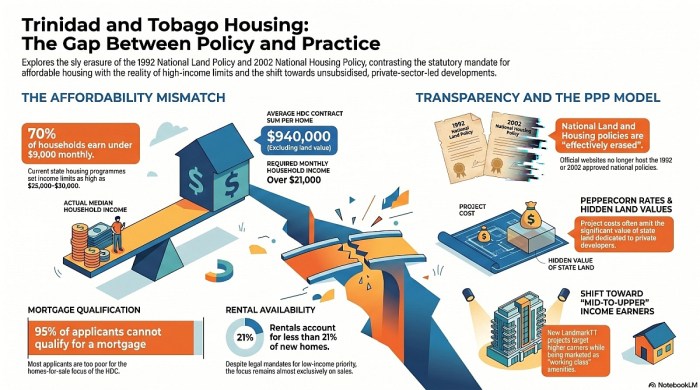

The CSO Statistics – 70% of our households have a monthly income of less than $9,000, according to the most recent CSO research (the 2011 census).

HDC Research – Many official statements confirm that over 95% of the applicants on the HDC’s waiting-list cannot qualify for a mortgage, simply because they are too poor. My research shows that only 21% of new HDC homes are available for rent. When one considers the Policy and Statutory requirements, we are witness to an unpardonable, ongoing misallocation of vast State resources of Land and Capital. This is a case of sly erasure, in which established public policy and statutory obligations were erased to facilitate routine violations by the responsible state agency.

Over 95% of applicants cannot qualify for mortgages, yet roughly four-fifths of new HDC construction is aimed at ownership rather than rental, so the State is structurally producing new homes beyond the reach of those applicants.

HDC’s decision to pursue this approach to the public housing program, in violation of its statutory obligations, has had the result of fortifying the position of the middle class, all at the expense of the lower-income citizens for whom these provisions were established. That is the class war at work in this large-scale program.

Having set the public housing background, the needs assessment issue must be engaged to understand how these projects, none of which could possibly have satisfied a proper needs assessment, could be compliant with OPR requirements. The only way that practice could prevail is if challenge proceedings issued to the OPR are limited to disgruntled competing contractors or party-political issues, which is exactly what is happening. Such challenges would never trigger a sober examination of the actual basis of these projects.

The OPR has an overarching responsibility to ensure value for money, but this analysis illustrates that, despite the encouraging engagement of challenge proceedings and the timely disposal of those, there is still a sobering gap in terms of achieving the established statutory targets. Even though no numbers are explicitly stated in the HDC Act, it is clear from this analysis that there is a major issue in terms of those statutory objectives being breached by these projects.

So what should be the OPR’s role in this matter? The clear objective of the policy is to provide affordable homes to lower and middle income applicants, yet that is not being achieved. The limited grounds upon which challenges are engaged is only a part of the issue here. More importantly, there is a way that a purely project-based approach to project review does not at all serve the wider public interest and in fact can permit this unacceptable situation to persist. If needs assessments are only being prepared with respect to particular projects, there is every danger that this quiet evasion of the HDC’s statutory obligations will continue, to the detriment of the lower-income citizens it was established to serve.

A legitimate housing needs assessment would necessarily compare applicant income distribution, mortgage qualification rates, rental demand, household size, geographic need, and long-term affordability before project typology is selected.

The OPR needs to engage this question since there is a clear prospect of Public Money being placed at peril since it is being spent in violation of the HDC’s statutory obligations. The stakes are high and we must be determined in developing a new understanding of the intersection between Housing Policy and the PPDPPA if we are to ensure ‘Value for Public Money’.

The calculated silence and erasure of our progressive public housing policy must be unmasked and resisted if we are to realise the ‘principles of social justice so that the operation of our economic system results in the material resources of the community being so distributed as to subserve the common good’, as cited in our Constitution. The HDC must serve our poorest citizens for whom these systems were created.

Some concerns have emerged on the concentration of a large number of land agencies and, of course, the newcomer, LandMarkTT Properties Ltd, into the portfolio of Land and Legal Affairs Minister Saddam Hosein. While it is true that there are now a large number of state agencies under this Minister’s control, I balance that against two perspectives.

Firstly, Trinidad and Tobago has always had severely oversized Cabinets, given our modest size, so as a point of principle, a large number of agencies under one Minister is not in itself offensive to good order. That would really depend, in my view, on the quality of the various Boards and Officials of those agencies.

Secondly, the OPR has a statutory role in ensuring compliance with the Public Procurement & Disposal of Public Property Act, which Minister Hosein expressly affirmed when explaining how these agencies will work together. See Govt clarifies Landmark TT housing model amid criticism – Trinidad Guardian.

Under the OPR rules, LandMarkTT Properties is required to publish all contracts awarded, but reportedly did not do so for that ‘Allamby’ contract until after the OPR’s formal request. That is the ‘thing’, but what is the ‘meaning of the thing’? Was it that those public officials knew of the legal requirement and just ignored it, or was it that those officials were simply unaware of that requirement? More to the point, which of those alternatives is worse? So why can’t this ‘Allamby’ contract be published now?

“…the State is not required to seek financing for any of these housing projects, as no public funds will be used for the construction of those houses…”

“…The developers will be required to fund the entire construction and infrastructural cost of the projects…”. (both citations are from pg 7 of that day’s Hansard)

Two questions need to be answered –

Firstly, what is the area and value of the State lands committed to this project?

Moving beyond ‘Allamby’, if we accept the express statements on LandMarkTT Properties along with the disclosed contract sum, these are investments of public resources in a part of the housing market already served by the private sector. That is ‘crowding-out’ of private sector developers, which really only ought to be done if there are strong externalities to justify the action.

To my mind, there does not seem to be any visible difference between the programs of the HDC and LandMarkTT Properties.

The LandMarkTT Properties’ contract, now under OPR review, and the HDC’s intended award of eleven contracts totalling $3.48 Billion to create 3,700 new homes are a continuation of the misguided public housing program under the 2002 National Housing Policy. That Policy finds statutory expression in the HDC Act (No 24 of 2005) at Section 13(1)(a), which mandates HDC to create affordable housing for low and middle income applicants.

Just consider the basic arithmetic, which shows us that those new HDC contracts would produce housing at a contract sum averaging $940,000.

[$3,480,000,000 ÷ 3,700 = $940,540].

Please remember that the land is never included in these announcements, so those sale prices would be in the $1.0M range, which would require monthly mortgage payments in the $7,000 range and a monthly household income in excess of $21,000. The most recent CSO research was the 2011 census, which showed that 70% of our households have a monthly income of less than $9,000. So, what are we really doing?

The issue here is that most of the HDC applicants cannot qualify for a mortgage, simply because they are too poor. At least 95% of those HDC applicants are in that predicament, while getting news of these huge new projects with no provision for any poor families. None for them. Despite the self-serving press statements and the utter abuse of the word ‘affordable’, the entire new program comprises new homes for sale. Not one new home for rent. There is an undeclared ‘cozy consensus’ between our political parties on this important issue, at least insofar as remaining silent on new homes for our neediest citizens.

That undeclared consensus can embolden public officials to make entirely bizarre statements. Just consider Minister Hosein’s reported statement to Parliament (p.6) on Friday, 15 May 2026:

“Under the PPP model, the State shall make lands available to private-sector investors and developers who shall, in turn, construct fully planned housing communities targeted at mid-to-upper income earners. These housing units will be situated in gated communities, with modern design and amenities to cater for the working class.”

So, ‘mid to upper income earners’ are now being openly portrayed as ‘the working class’. Well, I tell you eh.

Going further, there is a pregnant issue when one considers the intersection between these Housing Policy issues and the Public Procurement and the Disposal of Public Property Act (PPDPPA). The established learning is that Public Money is to be managed and accounted for to a higher standard than Private Money. That is fundamental in understanding the importance of high standards of Public Sector Governance. Our Housing Policy and its statutory root require that HDC dedicate itself to creating affordable housing for low- and middle-income applicants. Alongside those obligations in its originating statute, HDC is also required to comply with the PPDPPA and the OPR regulations. The PPDPPA/OPR mandates that every project, before it is advertised, must have satisfied a Needs Assessment, which requires the deep consideration of these questions: What are we doing? and Why are we doing it?.

Interestingly enough, that process is part of the internationally accepted Procurement Cycle used in both the Public and Private sectors.

When one juxtaposes the demonstrated Housing Policy dysfunction with the legal requirement for a Needs Assessment, it is inconceivable that those projects, which do not at all conform to HDC’s legal requirements, could have satisfied any proper Needs Assessment. Of course, it is open to HDC to show us otherwise, after all we are paying for the whole exercise, not so?

Thus far, our reports and debates on these issues have been confined to the usual claims of connected contractors, politically favoured players and allegations of improper behaviour. None of those issues are unimportant and they must be treated with due seriousness, but what is emerging here is the far more serious implications of our entrenched practices. The PPDPPA established ‘Value for Money’ as being fundamental, but if we are to recognise the moment for what it is, what we now need to develop and advance is the notion of ‘Value for Public Money’. We must explicitly behave as if Public Money is more important than Private Money, there is no alternative. We have to advance these concepts to properly defend the Public Interest.

Given that ‘cozy consensus’ between the political parties, we cannot expect these critical issues to be raised by any of those. Issues of this kind ought to attract the attention of our scholars at UWI and UTT, but here we are. Between a rock and a hard place, what a disgrace.

This is the first part of my two-part analysis of some fundamental and large-scale issues of the State’s Land and Housing Policies and Programs. This first part deals with the background, while the second part will deal with the unfolding issues on the Trinidad and Tobago Housing Development Corporation (HDC) and LandMarkTT Properties programs. This analysis is based on the relevant policies, laws, official statistics, and published statements.

Our country actually has a National Land Policy (1992) and a National Housing Policy (2002), both of which have been effectively erased by successive political administrations. So that is why none of the officials busily commenting on land and housing ever refer to our existing national policies. If one were to try searching official websites for those policies, it would be fruitless, far less to actually request those policies from one of the responsible State Ministries or Agencies. Our public officials make bold public statements, while we are witness to huge public investments in this critical arena, all without regard to the approved national policies. That is the framing for the collective fix that we are in, and this has been the case for over 20 years now, since the official policies became inconvenient.

I will demonstrate how the official land and housing programs have unfolded in an increasingly contrary manner when compared to the objectives of the official policies. Policy Review is a normal procedure to ensure proper alignment between objectives and outcomes. The problem in this instance is that a policy review would have required a full statement of the facts in terms of both spending and performance, together with public consultations. Those practices are serially avoided by successive political administrations, so the solution was to simply ‘erase’ those national policies from view and carry on regardless. This is the detrimental sly erasure which has ensured that those beneficial policies are effectively concealed from the public it is intended to serve. That is the background to the ongoing silence on our National Land and Housing Policies. I have kept those Policies, hence my continuing series of challenges.

The Land for the Landless program, which is handled by the Land Settlement Agency (LSA), needs a significant adjustment to its rules, since although that program was intended for those applicants outside HDC criteria, its monthly income limit is $30,000, while the HDC’s monthly income limit is $25,000. (Click here for Frequently Asked Questions on HDC website). Quite frankly, apart from the re-establishment of an LSA limit which is lower than the HDC limit, both those monthly income limits need to be greatly reduced to reflect reality. We often hear of fact-based decision-making as a desirable approach to complex problems, so the qualification criteria for these State land and housing programs must be reconsidered in light of the most recent CSO research (2011 census) showing that 70% of our households have a monthly income of less than $9,000. That means that the monthly income limits for these programs are far too high if the intention is to address the dire situation of the neediest households.

The actual household income levels in our country are so low that over 95% of the applicants on the HDC’s waiting list cannot ever qualify for a mortgage, simply because they are too poor. We set these unrealistic maximum income levels for applicants, and the result is plain to see. Most applicants cannot afford to buy, and yet we have a state housing program supposedly intended to assist the neediest families, which almost exclusively focuses on homes for sale. The HDC is a Statutory Agency, established by Act No. 24 of 2005. It is a creature of Statute and therefore bound to follow that law. Section 13 (1) (a) of the HDC Act requires it to provide “affordable shelter and associated community facilities for low and middle income persons”. That sequence is no accident; the very HDC Act gives precedence to the low income persons, it’s in the law. The income profile amongst applicants and the text of the originating Act gives priority to HDC building homes for rent in preference to homes for sale. Yes, that is the law, so what is the actual result? My detailed research into the current 2002 Housing Policy shows that HDC has never built more than 21% of its new homes for rent. Those findings are from 2003 to now, so the lack of focus and sheer misallocation of vast sums of Public Money spans several political administrations. In this one thing at least, there is some kind of unusual consensus between supposed political rivals.

Saddam Hosein, MP, Minister of Land and Legal Affairs

Public Private Partnership (PPP) approaches to housing provision are now in vogue, but we need to consider the extent to which that model can deliver the decent housing so desperately needed by our poorest citizens. In addition, while we note the Minister of Land and Legal Affairs, Saddam Hosein’s declaration that no State monies are to be spent on these projects, two issues arise. Firstly, there is a long-term and detrimental blind spot in how projects are discussed in our country in that we never, ever mention the value of the lands being dedicated to these projects so that the only figure mentioned is the contract sum for the construction. That needs to change – the State needs to explicitly declare the value of the lands being dedicated to these projects if we are to have a clear picture of the total cost of these developments. Secondly, the PPP agreements I have seen all have provisions that effectively inoculate the private sector party from any losses if there should be a shortfall in the projected sales. In such cases, the State is in fact guaranteeing the return of the private sector by removing those risks, so one is entitled to wonder just what risk the private sector is bearing. If the answer is that the private sector is bearing no risks, that means that we have been pursuing a detrimental PPP model, thus far.

Minister Hosein’s statements that the State has not contracted to make any payments within those arrangements needs to be carefully scrutinised. Firstly, as I stated earlier, we need to include the value of the land in our consideration of these projects, it is not possible to appreciate the full scope of these projects if we continue to omit the land value. That is also ironic given that the ‘Land and Legal Affairs Minister’ is going to be playing a leading role in these arrangements going forward. Secondly, apart from disclosing those previously concealed land costs, we also need to acknowledge that these contracts commonly allow private developers to get paid by the State if the projected commercial outcomes are not met. Quite simply, I do not at all accept the notion that no Public Money is at risk in these projects. It all comes down to the difference between the cash and accrual approaches to accounting and that can be a challenging matter for some people.

This is the recording of my session at the PC+ Tobago Public Procurement Laboratory, which was at the Magdalena Grand Beach & Golf Resort (MGBR) on Thursday, 27, and Friday, 28 November 2025. I presented on the first day on ‘PUBLIC PRIVATE PARTNERSHIPS: THE TOBAGO STORY’, in which I analysed the very venue (MGBR), the MILSHIRV project, and the aborted Tobago Sandals proposals.

The State’s provision of affordable housing to low and middle-income applicants has been delivered primarily by the Housing Development Corporation (HDC) and, to a lesser extent, the Land Settlement Agency (LSA).

The current Housing Policy—”Showing Trinidad & Tobago a New Way Home“—was established in 2002 with the ambitious target of producing 100,000 new homes within a decade. Before the HDC was established in 2005, that role was fulfilled by the National Housing Authority (NHA), which was established in 1962. Despite allocations of public money and private sector borrowings exceeding $20 billion since 2002, the NHA/HDC completed less than 25,000 new homes.

Beyond the gross totals and their serious implications lies a more insidious issue: the actual effectiveness of this large-scale public housing program when we consider the human element. The HDC Act stipulates that its purpose as a statutory agency is to facilitate affordable housing for low and middle-income applicants. Yet over 90% of applicants on the HDC waiting list cannot qualify for a mortgage because they are simply too poor, while only 21% of new HDC homes are available for rent. Given the amounts of public money invested in this program and the desperate housing needs of our poorest citizens, this represents a tremendous misallocation of scarce resources.

The HDC’s low output compared to original targets, combined with its failure to serve the majority of applicants for affordable housing, constitutes a serious indictment of its performance.

Since 2003, NHA/HDC has not had audited Financial Statements, so there are substantial financial accountability issues in addition to those noted earlier. HDC stated that the financial statements for 2003 to 2009 were audited, but those financial statements were accompanied by Independent Auditors Reports, issued by KPMG Chartered Accountants, every one of which was subject to a Disclaimer of Opinion. The Disclaimer of Opinion is many times worse than a mere qualified audit since it means that the auditor has so little confidence in the records that it is impossible to form a responsible professional opinion.

During the recently concluded election campaign, I was astonished by Jearlean John’s promise to deliver 500 new homes per week and “…we are looking to build at least 10,000 houses per year…” if the UNC were elected. Ms. John served as HDC’s Managing Director from November 2009 to March 2016 and provided serious assistance to my public housing research during that period. There is no doubt that she is well-informed on these matters.

The Housing Ministry now has a Minister and two Ministers of State—a considerable commitment of political capital to this important public policy area.

We must avoid the errors of the past if we are to do better. If the newly elected UNC Administration wishes to succeed where others have failed, it must act fundamentally differently from the previous PNM government.

In the early 2000s, the then-PNM administration, under the late Patrick Manning, made ambitious urban development proposals intended to reduce the State’s historic dependence on private-sector landlords.

That program was executed by UDECOTT, under the hand of Calder Hart, with 2.3M square feet of offices constructed by the State in POS. The iconic, elliptical, blue-glass office tower on Independence Square is Nicholas Towers, which contains 100,000 sf of offices – so our Public Money funded the construction of new offices 23 times the size of Nicholas Towers.

Apart from the staggering UDECOTT corruption confirmed at the 2009 Uff Enquiry, I have always had nagging doubts as to whether that massive office construction program actually achieved its objectives. Despite my efforts, it was never clear if our monthly rental bill for State offices had in fact been significantly reduced as a result of that UDECOTT program. There certainly have been no official declarations of that achievement, which one would expect if indeed that had been the case, given our political culture.

In October 2023, I exchanged points with then Public Administration Minister, Ms Allison West, on the conflicting and incomplete details of the State’s leasing of the former RBC HQ building at Park St in POS for the Office of the DPP. At that time, then-Minister West attempted a rebuttal of my claims of massive corruption, but that was rendered nugatory by both her failure to provide any substantiation for the details of the Public Monies spent on that failed project and her claims that all the details of State leases were available on the ‘Property & Real Estate portal’ at https://pmis.gov.tt/. That link remains a dead one, so the information is as yet inaccessible to the public. At that time, I asked the question –

‘Why not make the entire database readily accessible to the public, just like the EBC list?’.

There was no reply, so no details were provided.

I was therefore pleased to hear the statement by Prime Minister Kamla Persad-Bissessar SC to the 22nd May 2025 post-Cabinet Press Briefing in which the issue of secrecy/confidentiality of State office rentals was specifically addressed –

“…We will release the existing list to the Public, in the interest of Transparency…this is your Money, this is Taxpayers’ Money, and you have a right to know where your Money is being spent…So Minister has been given the authority to release that list of the rentals, for you to see what has been happening, in secret and, in some cases, illegally…if public members don’t want people to know that we are renting your building, Government is renting your building, with Taxpayers’ Money, then too bad for you, don’t rent-out your building, do not rent-out your building if you don’t want people to know that you are renting your building to the Government…simple as that, so don’t come and cry and plead ‘privacy’, there is no privacy when we are spending Taxpayers’ Dollars…there can be no defence of ‘Privacy’, or you don’t want your name out there…”

I entirely agree with those emphatic statements from our PM, Kamla Persad-Bissessar SC, so I am calling for all the details of the State’s office leases to be published as a searchable database showing Addresses: Owners’ identities: Square footage: Carparking: Rental paid: Lease terms (i.e. start and finish dates): Repairing/Maintenance obligations.

The implementation of the controversial Property Tax is now underway in Trinidad and Tobago, marked by a series of official announcements and the issuance of revised Notices of Valuation to an estimated 400,000 residential taxpayers. While these revisions are necessary, there is a critical flaw in the system that must be addressed: the restricted access to the Valuation Roll database. This column explores the implications of this restricted access, argues for the necessity of transparency, and identifies who stands to gain from maintaining the status quo.

The new Property Tax system in T&T aims to deliver equitable taxes through a crowd-sourcing approach, which promises transparency and low operational costs. Property owners were asked to submit detailed returns – about 60,000 of which were sent – which were then analyzed by the Valuation Division of the Finance Ministry. Selected properties were inspected and measured, leading to provisional tax assessments. Taxpayers have the right to object to these assessments, which would be refined through this iterative process of public feedback, ensuring fairness and accuracy.

Afra Raymond, Managing Director of property advisory company, Raymond & Pierre, speaks at the company’s 50th anniversary celebration, a mini-Conference on Land and Property in Trinidad and Tobago, hosted at the Centre of Excellence on Tuesday 13th December 2022. His first topic there was ‘Public Procurement law through the lens of professional responsibility‘. His second topic there was ‘Land & Housing Policy in post-Independence Trinidad and Tobago‘ that sees to the needs of poor people.

Programme Date: 13 December 2022

Programme Length: 00:16:02 and 00:12:38

Playlist contains 2 videos. Select in top right corner.

The Ministry of Trade and Industry (MTI) responded on Sunday, 18 June 2023 to my letter of Friday, 16 June 2023, which pointed-out that the Minister’s reported statement that Trinidad Hilton “had not been renovated for over 20 years” was entirely untrue.

The MTI’s second paragraph confirmed my statements that Trinidad Hilton had been extensively renovated in a program which commenced in 2008. The rest of the MTI’s letter set out some details of the works which are now proposed for that property, but while it is good that we now have that greater level of detail, some serious questions now arise.

My analysis of the Trinidad Hilton, given the estimated profits, as derived from the reported payments of Corporation Tax, shows that the payments of Rent to eTecK would be –

Year

Net Profit (after tax, consistent with AGOP)

Rent @76% of Net Profit

Return on Investment ($634M)

2015

$3.099M

$2.355M

0.37%

2016

$6.233M

$4.737M

0.75%

2017

$2.533M

$1.925M

0.31%

2018

$1.987M

$1.510M

0.24%

These estimates indicate extremely low rates of Return on Investment, which no private sector investor would tolerate, especially given the ongoing requirement for expensive periodic capital works.

The concerns all relate to the investment decision, given that the State owns the three largest hotels in T&T – Trinidad Hilton, Hyatt Regency and Magdalena Grand in Tobago.

Since the MTI has engaged in this much-needed disclosure, it would be in the public interest if these details could be now provided –

Comparison – without details of the parts renovated in the 2008 program and the out-turn costs, it is impossible to discern the rationale for these new works. I am requesting that MTI provide those details to permit the comparison to justify the new investment;

The impact of Hyatt Regency – Hyatt Regency caused a virtual collapse in the POS Hotel market since its opening in Jan 2008, with severe impacts on other hotels in our capital city, as a result of the Government diverting most of its functions/conferences to that new venue. The affected hotels include Ambassador; Crowne Plaza; Kapok; Cascadia; Carlton Savannah and most of all the Trinidad Hilton which decisively lost its pre-eminence in the POS market. Did the 2008 program of works have the effect of improving Trinidad Hilton’s fortunes? What has been its occupancy rate in the past 15 years? I recently saw elaborate proposals for the redevelopment of the Salvatori Building site in downtown POS as a Public Private Partnership, to include a 319-room hotel – how does this affect the investment decision?;

Financial performance of the State-owned hotels – this area has been a virtual Black Hole, with very little, if any, reliable information made available. Our Public Officials observe a serious, detrimental commitment to silence on the performance of these massive investments. No audited accounts have ever been made available for these State-owned hotels, although we know that the foreign companies with Management Agreements (Hyatt, Hilton and Hospitality Solutions International for Magdalena Grand in Tobago) would have regular and proper accounts showing real returns to justify their continued operations. Once again, I am requesting MTI to make these figures available to the public, who are paying for all of this.

The Department of Management Studies at the Faculty of Social Sciences at UWI St Augustine offers post-graduate studies on Tourism and Management, so it would be interesting to have their input on these large-scale investment decisions.