![]() This week I will provide further necessary correctives on the impending re-introduction of the Property Tax, which is not a new tax. It previously existed as House Rates in the five cities and Land & Building Taxes in the other parts of the country.

This week I will provide further necessary correctives on the impending re-introduction of the Property Tax, which is not a new tax. It previously existed as House Rates in the five cities and Land & Building Taxes in the other parts of the country.

Tax Evasion

Self-employed and professionals and sole traders have always under-reported their earnings and never paid the correct taxes. Those people often use property as a useful place to store their untaxed wealth. We have never really dealt with this tradition of tax evasion amongst our successful citizens and I cannot remember anyone being imprisoned or having property auctioned due to taxes owed. Whatever my doubts about the motivation of the American Imperium in pushing its ‘anti-tax haven’ agenda, some things do give cause for a pause. For instance, the Financial Times article of 28 June 2017 – ‘Trinidad & Tobago left as the last blacklisted tax haven‘.

The new Property Tax system will require a open database of all property holdings if it is to be effective. The tax evaders are usually hostile to any moves to make their affairs visible, so I would not be surprised to hear increasing objections about crime, kidnapping and so on as justifications for somehow continuing to shelter these peoples’ affairs from scrutiny. Of course when one considers the commonplace flaunting of wealthy people, it is impossible to take those protests about the fear of crime seriously. Everyone knows who are the wealthy people, they make sure we all know, so the real fear is the fear of paying their fair share.

There are really substantial flows of rentals and other property income which is untaxed, so the open database of the new Property Tax system is a big threat to those interests. Hence the growing, frantic objections.

Improvements

The question of improvements arose last week in a comical Parliamentary exchange with the Opposition Leader asking if dog kennels/duck ponds/fowl coops would also attract Property Taxes. The Minister of Finance gave a circular answer which did not in my view clarify this aspect of these valid public concerns.

The simple fact is that an improved property will be more valuable than an unimproved one. Take the example of two houses alongside each other of identical age, design, condition, land area, building area, number of bedrooms/bathrooms. If one of those houses is substantially improved, it stands to reason that its rental value will be greater than the unimproved one. Without getting granular as to the exact value of a duck pond or dog kennel, the case for a difference in rental value is as clear as it is irrefutable. Any fair professional valuation of those properties would recognise the differences in rental values attributable to the improvements.

I can only see one reasonable case to negate that sound assumption that improvements add value. That would be in the case of an idiosyncratic improvement, which was purely to an owner’s taste and preference but which did not attract any real interest in the market for that property. Naturally, those would be very limited cases.

Local Government Funding

One of the important issues in relation to the Property Tax is that the current proposals are for those monies to go into the Consolidated Fund, which is directly under control of the elected government. The previous system was one in which property taxes were paid to the local government bodies and therefore formed part of their funding, collected with a degree of autonomy.

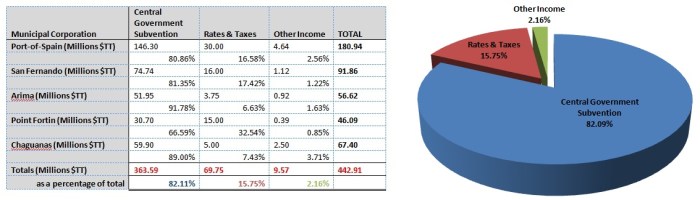

The actual relationship between these streams of funding is portrayed in this graph and table, derived from actual payments in Ministry of Finance records. 2009 was the last relevant year for which those records were kept, since the property tax collections were halted then.

From the official records, just over 82% of the cost of running our five cities was funded by central government, with just under 16% being derived from house rates. The first point therefore being that a small fraction of the actual cost of running a city could have been funded by property tax, at 2009 levels. The second point, is that if property taxes increased as per the Ministry of Finance projections there would be a greater degree of autonomy if those funds were collected at the local government level.

In 2009, $143M was collected in property taxes and the official 2017 estimate was for $503M to be collected, which is just about 3.5 times more. All other things being equal, if one applied that kind of increase to the 2009 figures, it is feasible that about 55% of the cost of our cities could be met from Property Taxes, if those funds were collected directly by the respective local government bodies. That is all the more reason to continue to lobby for those funds to be collected directly by those bodies.

The UNC Record

Finally, I have to say that the record of the UNC on this issue has been a poor one. As detailed in the previous article, during the UNC’s 1995-2001 term in office the collections of Land & Building Taxes collapsed from $109M in 1994 to a mere $61M in 1995 and bumping along at that parlous level until 2002, when $94M was collected. As a practitioner, I am unaware of any prosecutions of any property owners for non-payment and of course, one is not suggesting that that those non-compliant property owners were UNC supporters. It is just striking how badly that portfolio was handled during that first UNC term in office.

The second UNC term was actually more sobering, in that the party had 29 seats and could have reviewed or repealed the Property Tax Act of 2009 if its objections were that serious. Instead, the UNC marked time during its five years and three months in office. Having lost the September 2015 elections, we are now experiencing UNC puzzlement in Parliament and legal challenges evermore. I tell you.

“The new Property Tax system will require a open database of all property holdings if it is to be effective.”

You keep saying this, but I’ve never seen or heard it anywhere else. Did I miss something?

Sections five to nine of the Property Tax Act (No 18 of 2009) refer to the Assessment Roll which is the database – the Act is here – http://rgd.legalaffairs.gov.tt/laws2/alphabetical_list/lawspdfs/76.04.pdf

This roll might be similar to how land title are held in the registry?

We cannot know for sure, but yes, I expect it to be a similar setup in terms of online access – I do not think they can or will charge for access, though…

Given our cultural aversion to transparency, I hope that you are right.